As we formally say farewell to 2025 and move forward in 2026, we want to take a moment to reflect on what has been a year of notable growth for Community First Credit Union. The past year brought meaningful progress on our key initiatives, culminating in the successful execution of our welcoming of new members in southern Humboldt County and the completion of the merger of Vocality Community Credit Union with Community First.

Despite a complex and volatile operating environment, we delivered strong financial performance and continued to build a stronger and more resilient credit union for the future. None of this would have been possible without the dedication of our team and the continued trust of our members.

The Economic Landscape and Industry Outlook

Heading into 2025, expectations for interest rate cuts were modest. While we anticipated modest movement, the Federal Reserve ultimately implemented three rate cuts totaling 75 basis points late in the year. While these actions steepened the yield curve and resulted in a more normalized shape, the changes were more pronounced in the short to intermediate sections of the curve.

Short-term rates declined more meaningfully, while longer-term rates that impact mortgage financing costs dipped more modestly. Mortgage activity continued to face headwinds driven by affordability challenges, elevated home prices, and inventory. These dynamics remain largely unchanged as we enter 2026.

Auto lending faced similar affordability pressures. While rates improved slightly, vehicle prices and related costs of ownership remain at historically high levels. Longer auto loan terms have become more prevalent, reflecting the broader affordability challenge faced by consumers. Inflation moderated modestly during the year, while unemployment increased slightly, leaving monetary policymakers in a difficult position as they balance economic growth with price stability. Ongoing geopolitical tensions and fiscal policy uncertainty continue to contribute to a highly volatile operating environment.

In this environment, our approach remains consistent. Stay disciplined, continue to invest in our members and communities, prudently manage the balance sheet, and focus on long-term value for our members.

2025 Financial Performance

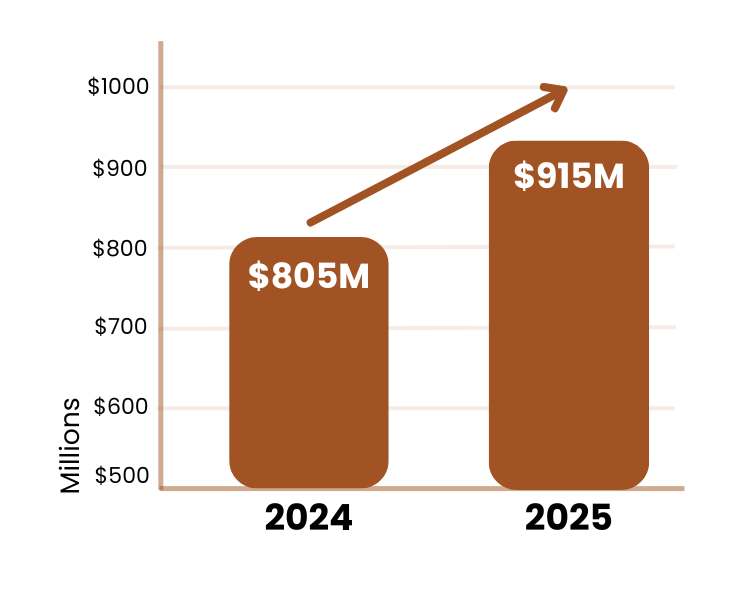

2025 was a strong year financially for Community First Credit Union. We ended the year with total assets of approximately $915 million and net income of $4.83 million. Return on Assets finished at 0.56%, significantly exceeding our original budget expectations. Net interest income performed well above plan, driven by strategic asset deployment.

We made substantial progress in rebalancing the loan portfolio, reducing our concentration in auto loans from 56.8% at the end of 2024 to 43% at the end of 2025, while increasing diversification across other lending categories.

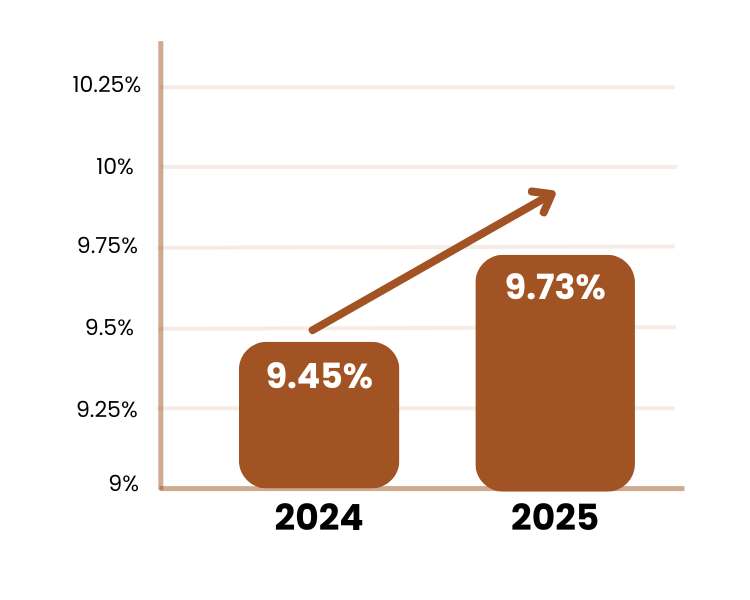

Funding costs improved over the course of the year as deposit pricing normalized. Non-interest income improved to $8.7 million and operating expenses finished right on plan at $35 million despite one-time non-recurring costs associated with the merger. Importantly, our regulatory capital position strengthened significantly, improving to 9.73%, enhancing our fiscal durability for the future.

Overall, 2025 was a year of strong growth and disciplined financial execution.

Strategic Highlights and Execution

Beyond financial performance, the most significant milestone for 2025 was the successful completion of the merger of Vocality Community Credit Union with Community First. This was a complex undertaking that required rigorous coordination across the entire organization.

The integration was executed very adeptly and seamlessly due to the outstanding work of our team. The benefits of greater scale, expanded membership, and broader geographic reach in the North Bay are already evident.

We'll note a few of the other key initiatives we completed in 2025:

- Implemented new software and model methodologies to improve the estimate for future loan losses, strengthening our capability to offer outstanding financing rates to our members.

- Finalized new debit and credit card processing and brand agreements that will reduce operating expenses, enhance member card benefits, and result in greater levels of charitable giving in our communities.

- Implemented new technology and process improvements to help members when falling behind on their loans.

- Continued to make sizeable investments in new digital banking capabilities and our information security program.

- Expanded our product offerings, including a new residential jumbo portfolio product. Our Rapid Dough loan continued to grow and provide essential financial assistance to our members at a lower cost and with more favorable payment terms than predatory payday lenders.

- Expanded our Contact Center hours for greater member convenience and service.

- Modified and eliminated a number of legacy fees, including dramatically reducing member fees for overdraft protection.

Additionally, we increased our commitment to community impact, including record charitable contributions to support local philanthropy in our communities.

These efforts reflect a continued commitment to building a stronger credit union for our members and communities.

Looking Ahead to 2026 and Beyond

As we move forward in 2026, the operating environment remains highly volatile and uncertain due to a number of factors, including heightened domestic and geo-political tension. Community First will continue to focus our commitment on our members and communities as a trusted local cooperative in the North Bay.

We'll note some of the key initiatives we have planned for 2026.

- A $4 million(+) investment into a new charitable donation investment account to generate higher long-term investment yields that will allow us to enhance our philanthropic giving.

- Implementation of a new agreement with Mastercard to provide greater benefits for debit and credit card holders. In conjunction with and to celebrate with that new partnership, which we expect to go live this summer, Mastercard and Community First will be making sizeable new philanthropic investments in our communities.

- Sizeable investments in new Digital Banking capabilities, including more streamlined and convenient ways for members to open new deposit products digitally.

- New technology that dramatically reduces the time and ease for opening new memberships both digitally and in our branches.

- New Contact Center technology to enhance convenience for members when they call for information or assistance. This capability will be available 24 x 7, 365 days a year.

- Sizeable investments in new technology infrastructure to improve and enhance our resiliency.

- New investments in our information security program to enhance our information security resiliency.

Closing

As we look forward, we want to thank our team members for their hard work and commitment, our Board and Supervisory Committee for their leadership, and most of all our members for their continued trust in Community First. Your trust allows us to remain “Here For Good” and “Here for You” and all the communities we call home.

.jpg)

.jpg)